Inflation: Economic Enemy Number One

October 06, 2025; most recent update: May 16, 2026

Table of Contents

1. Essence of Inflation

2. Objects of Inflation: Item for Sale, Buying Charges, Currency

a. Pricier Items for Sale

b. Higher Buying-Related Charges

c. Weakening Currency

3. Everyone is a Buyer = Inflation Tends to Spread

4. Worse Environment for Consumers & Businesses

5. Greater Chance of Tax Increases

6. "Some Inflation is Good, Deflation isn't": Whys & Refutations

7. Anti-Inflation Factors & Why Inflation is Hard to Predict

Essence of Inflation

Inflation is usually understood as a situation when prices on average increase in an economy, whether globally, nationally, statewide, more locally, or any other way we decide to slice the geography. Given the constant flux and diverse economic conditions that occur within any of these areas, there are clear advantages in taking a macro view that summarizes the economy as a whole.

But there's a little bit of lie in this simpler, more intelligible view of inflation. For example, if significant inflation is confined to a county, it would be hard to convince residents there that it there is no inflation merely because prices have been stable at a broader level, such as in the state or nationally. The "big picture" wouldn't capture their picture.

Likewise, if thread costs increase tenfold, companies involved in sewing probably wouldn't agree that "the prices of things have been stable across the economy" even if they generally have.

When we ask if inflation exists, we should keep in mind: inflation for whom and for what?

So, from this vantage point, it's better to understand inflation as simply when the price of something increases. It can happen at any level of magnification: from an individual item for sale, to a product, to a good, to several goods, to all goods (and services); or from an individual seller, to several sellers, to all sellers in the economy.

It always, in some sense, implies a weakening of the currency relative to the item or items for sale. To use a common phrase, the currency has "less buying power" than before. If a pound of wheat costs $1 in January and $1.50 in February, then each unit of currency buys less of that same thing than before; it takes more units of the currency to buy the same thing.

But suppose the January price is $1 and the February price is $.90. That wouldn't necessarily mean that inflation is negative. For if the sales tax jumps from 5% to 20% in the same period then the final price would be $1.05 in January and $1.08 in February. So, in one sense, the currency would be strengthening relative to wheat but overall it would weakening -- at least where the sales tax went from 5% to 20%.

Deflation is a related concept, referring to when prices generally decrease. For this article, it will also refer to when the price of any item decreases, regardless of whether prices are falling overall.

Objects of Inflation: Item for Sale, Buying Charges, Currency

Inflation revolves around three objects (i.e. fundamental causes): the item for sale, any charge attached to its purchase, and the currency used for buying it. In turn, each fundamental cause can itself have different causes. But there are still just three basic causes of inflation.

Inflation can occur when the basic price of the item increases, when any charge for buying it increases, or when the currency for buying it weakens. However, none of these conditions independently guarantee inflation; rather, inflation happens in the total context of all three objects. For instance, if the basic price of an item increases but sales taxes decrease and the currency retains the same strength, the final price might end up being the same or lower than before despite the higher basic price.

Pricier Items for Sale

The before-tax price of an item for sale has many factors that can increase it.

[More Regulations]

------------------

Many types of regulations increase the cost of doing business. As more of these regulations occur, the increased business costs will often be reflected in the before-tax price of sales items.

[Non-market Events]

--------------------

Many non-market events can also increase business costs -- usually, but not always, by some type of property damage or loss. Natural disasters, war, social turmoil, and lawsuits are some common examples. Solving some non-market events can also increase business costs. For example, social turmoil or retail theft might increase business expenditures on security or surveillance.

[Overexpansion]

----------------

Sometimes a business expands its operations beyond what the market can support. Unable to recoup the short- and/or long-term costs of its expansionary investments, it must raise its prices or go bust.

[Diseconomies of Scale]

-----------------------

Another unintended consequence of expanding operations can be diseconomies of scale. In diseconomies of scale, even though more units are produced, stored, transported, or bought than before, the per unit cost of doing at least one of those activities increases rather than decreases. It happens when variable costs increase faster than output; variable costs are divided by proportionately fewer units than before, thus the per unit cost is a higher number. This is usually due to some type of ineffiency acquired as operations get bigger.

[Supply Shortage]

-----------------

A supply shortage simply means that supply cannot meet demand. This can be from an increase in demand, a decrease in supply, or both.

When supply decreases and demand remains the same, the environment is more fitting for sellers to set a higher price. Buyers are more willing to pay it since their options are more limited and the situation is more desparate. The same point applies when supply stays the same or increases but demand increases relative to it. (This doesn't necessarily mean that sellers will profit more than when supply is more abundant or at least more abundant relative to demand.)

But a price increase when supply falls isn't simply due to seller opportunism. Many times it's also because a seller must raise the price when inventory retracts. When a seller has less inventory, fixed costs and the lowest acceptable profit are divided by fewer units. (See economies of scale and seller economies of scale.) If the supply shrinkage is big enough, this means it is mathematically impossible to offer the same price as before and thus the per unit price must increase. The only other options are for the seller to take a loss or fall short of making a personally acceptable profit.

Many things can cause lower supply, such as factories shutting down or decreasing production due to natural disasters, war, social turmoil, or sudden unavailability or scarcity of an input that has no real replacement.

Supply shortages can also be caused by excessive money printing. There's an old saying that inflation is "too much money chasing too few goods." When the issuer of a currency (usually a government) overprints a currency, it means that the amount of currency becomes proportionately larger relative to the goods and services available in the market -- usually, but not necessarily, as a result of the currency production outpacing production of those goods and services. This eventually leads to more scarcity as the excess money supply makes its way through the economy.

[Costlier Replacement Inputs]

----------------------------

Sometimes the materials of a manufactured product become scare or are found to be unsafe or otherwise undesirable, and the materials replacing them are more expensive.

[Trends Towards More Expensive Goods]

---------------------------------------

As technology becomes more advanced in certain kinds of sales items, the price tends to increase. Military hardware is a prime example. For instance, the price of modern fighter jets, even when it comes down with economies of scale, is vastly more than the fighter jets of decades past since the technologies and complexity have increased enormously.

Higher Buying-Related Charges

Any type of fee or sales tax adds a purchasing cost to buyers, on top of any cost increase that may be happening with a certain item or type of item. Government taxes and fees, or any charges from parties processing the transaction are the most common examples.

Weakening Currency

Inflation can also happen because of issues with the currency itself. This is different from the inevitable effect of the currency weakening when an item for sale increases in price or purchase charges increase. When the currency itself weakens, it becomes less valuable independent of any price changes in the item for sale or purchase charges.

To be clear, a currency is simply whatever someone uses to buy things. It's primary role is as a medium of exchange. Therefore, in understanding a weakening of the currency itself, there are three key issues: a depreciation in the physical units of the currency, a decline in its acceptance or demand as a medium of exchange, and devaluation.

Just as with inflation related to the item for sale or charges attached to its purchase, currency weakening can happen at any level of magnifcation: globally, regionally, nationally, or more locally.

[Depreciation of Physical Units]

------------------------------

In the past, when currencies were made of valuable materials, a currency could weaken simply due to changes in the physical nature of the units. The psychological principle behind this is timeless even though currencies have evolved from being commodity based. For instance, if a currency originally of silver coins becomes diluted with less desired metals over time, sellers will tend to demand more coinage than before for the same thing (e.g. two coins for a pound of wheat rather than one coin). This behavior is due to an axiom of economics, "economic rationality": people try to achieve the highest benefit to cost ratio when two or more economic options exist. Since each coin has less value than before, sellers will likely give buyers the same thing -- i.e., "pay" the same cost in exchange -- only if the quantity of coinage is larger, in order to obtain the same benefit (value) for their cost as before. Therefore buyers will get only half a pound of wheat for each coin rather than the full pound previously.

Another way to look at this is that an individual seller, realizing its sellers will find the newer coins less appealing, calculates that the other sellers would be more likely to accept them if they simply get a larger quantity of the lesser metal as compensation for its inferior quality.

Governments could still ban such practices and mandate that the newer coins be recognized as equal to the older coins, but this wouldn't change the basic fact of economic rationality, which would still play itself out even under government mandates. For instance, sellers might give buyers the "same thing" as before for one coin, but of a lesser size or quality.

[Decline in Acceptance or Demand]

----------------------------------

The most important factor of a currency is its degree of acceptance as a medium of exchange, since its primary role is as means of payment. Its second most important role is as a store of value. But the second role depends on the first: a currency's value isn't based on what it is physically made of but the degree to which it is accepted. What people mainly care about is that they will get the goods or services sought when they use a certain currency. So, historically, gold and silver coins haven't been valuable because of the metals that comprise them but because people want those materials and are therefore willing to accept such coins as payment. No material actually has this or that amount of value intrinsically; people determine each material's value.

Thus, when a currency's acceptance declines, it means that people have less faith that others will accept it as a means of payment. Consequently, its value (what can be obtained with it) declines as well. A currency can still be widely accepted even with an eroding value, but tends to rapidly lose acceptance when its value declines significantly within a relatively short time.

What kinds of things cause a decrease of faith in a currency? A depreciation in the physical value of the units, just mentioned, would be one. Another is the absence or loss of convertibility, which in turn is connected to collateral.

The less a currency can convert into other mediums of exchange, the less it is desired, since the user of the currency is more at risk of significantly losing wealth if the currency were to rapidly lose value. Also, the user has fewer buying opportunities since a seller may want a medium of exchange other than the buyer's currency and one that the currency cannot be exchanged for.

The most trustworthy route of conversion is by going straight to the source: the issuer's collateral. Even though conversions by a third party are possible, they are less reliable and riskier, especially in times when users of a currency are eager to get rid of it. Unlike third parties, the issuer has an interest in converting even when the currency's value is plummeting and will likely be worth even less after the exchange: salvaging their, and the currency's, reputation -- among other things. But if the issuer has insufficient or unacceptable collateral (unlike, say, gold or silver), then the user of the currency is possibly left with a situation where the currency's value is merely in its regional or local acceptance as a means of payment. Like coin tokens at some arcades or amusement centers, the currency's usefulness would be limited to where it's accepted, with no return option allowed.

The conditions of acceptance just described pertain to a world of the not too distant past. Until fairly recently in history, paper currencies were backed by valuable metals such as gold or silver, meaning each unit of currency was officially worth a certain amount of a valuable metal and redeemable for that metal quantity. This model of currency is called "representative money."

In the current world of fiat currencies, where none of the paper currencies are backed by commodities, the issue of convertibility is still important (e.g.1 and 2) but collateral is not. However, a global return to representative money can't be ruled out, especially with the growth of stablecoins backed by precious metals and BRICS nations considering their own currency backed with one or more commodities.

Today, trust in the currency isn't ultimately grounded in the collateral the issuer has but in the credibility of the issuer themself. But many of the same criteria of credibility of the past apply today.

In the past, if a nation's actual gold or silver reserves were believed to be inadequate for converting all of its currency back to them, fewer people would want the currency, seeing the risk involved. This wouldn't necessarily lead to a run on the currency but clearly would be a factor making the currency less appealing. Skepticism that the reserves were, or would later be, adequate might happen if the nation incurred large debts, failed to make payments, or was in the midst of political turmoil.

Now days, a high level of creditworthiness is like physical collateral in that it is an assurance -- though of a lesser kind -- that holders of the currency won't lose their wealth, since it makes it less likely that the currency will be unstable and thus lose significant amounts of value in a short time. With quick, significant drops in value, users of the currency have less time to adjust to, and combat, the decreases in wealth via investments or other means. Real, long-term wealth loss is therefore more likely. As with trust in the nation's reserves, things such as national debt, monetary and economic policies, and the degree of political stability are factors that play into creditworthiness.

[Devaluation]

-------------

Implied in the previous two subsections is that a government can pursue policies that indirectly affect its currency's value, by increasing or decreasing its desirability in the market. A government might, for example, narrow the number of other currencies it can convert to, resulting in a less appealing currency.

But a currency can also weaken from direct government action. In today's age of fiat currencies, nations often weaken their currency relative to others mainly to make the price of exports relatively cheaper and imports more expensive, thus strengthening their trade position between nations and often as an attempt to lessen trade deficits.

Everyone is a Buyer = Inflation Tends to Spread

One reason inflation is the main threat to the economy is the universal effect it has or can have on everyone. Everyone is a buyer: individual consumers, organizations, businesses, and governments. It is the one unversal role in the economy. Not everyone produces goods or sells goods, but everyone buys them -- at least indirectly.

Because of this universal aspect, inflation has a tendency to spread. This is partly because the extra expenses for each buyer will likely reverberate far beyond just their purchases of the initially pricier goods.

That last point is evident by the basic fact that others are likely to pass their inflation on to you. For instance, when things cost more at the store or the gas pump, you're also more likely to get a higher bill from the plumber, electrician, and anyone else providing you goods or services. Maybe not at first, but this has a greater chance of happening eventually. And let's say you're a barber or beautician. Now there would be even more financial pressure and incentive for you to raise your prices too, since you would be getting hit from more directions than before. So inflation has a tendency to spread from the initial goods or services from which it began to other goods and services.

How much inflation will spread depends partly on how bad the initial source of inflation is. Is the inflation isolated to just a few goods or services or many? Are those goods or services major underpinnings of the economy or not? Is the initial inflation a relatively small price or tax increase, or is it a fairly large one? Nevertheless, regardless of the severity of the initial inflation, inflation tends to spread.

Therefore the common belief that "a little inflation is good" is mistaken. A little inflation tends to lead to a little bit more inflation and, as the pressure builds, a little bit more inflation after that.

This will be explained in greater detail in the following sections.

Worse Environment for Consumers & Businesses

The impact of inflation throughout the economy is best seen by looking more closely at how it affects consumers and businesses. The relationship between consumers and businesses is circular rather than one-directional and therefore how each is affected by higher prices can't really be separated into independent sections. When one is affected, it has a potential impact on the other, in a virtually endless cycle. Nevertheless, the process is pretty straightforward.

First, what is the immediate impact on many businesses when prices go up? Higher general prices means business expenses will likely increase not just for inputs or merchandise, but other business costs as well (inflation tends to spread). Thus it becomes more likely that their prices will increase beyond just the higher costs of producing or acquiring the products sold.

Also, as inputs and merchandise become more expensive, the volume a business can buy decreases, possibly reducing inventory and further raising their prices since fixed costs and the lowest acceptable profit would be divided by fewer units than before.

With a general rise in prices, a significant number of consumers are likely to spend less. When this happens, many businesses will see decreased profits at a time when costs are going up, increasing the chances of layoffs, reduced worker hours, or less hiring. That, in turn, would add to the diminished consumer spending throughout the economy.

But even for those who don't experience layoffs or reduced hours, the higher prices mean that fewer goods and services exhaust consumers' money (generally) and that their money has a shorter reach throughout the economy. That alone means that fewer businesses are likely to succeed compared to if the economy has lower prices generally.

Finally, not only will individual customer revenue likely decline but revenue from other businesses as well, as many or most businesses are likely to spend less.

Greater Chance of Tax Increases

First, since governments pay for building-related and other materials, any increase in the cost of those things makes a tax increase more likely.

Secondly, if the economy begins to slow because of that same inflation -- which it likely will -- then there is even more pressure on the government to raise taxes. Decreased consumer spending hurts sales-tax revenues, and the increased need for government assistance as employment and worker hours decrease put additional strain on government budgets.

And as government taxes increase, that simply adds to the inflation already in the economy. It doesn't matter whether the tax increase is a sales tax or some other. Either way, it means some people or people generally have less money to make ends meet; either scenerio makes an extra round of inflation more likely. It's not hard to see the potential of a virtually endless cycle of inflation.

This is a good example not only of how inflation tends to spread, but that the more it spreads, the greater chance it has of spreading even further.

"Some Inflation is Good, Deflation isn't": Whys & Refutations

Current, mainstream economic thought is certainly aware of the damage that inflation can do. But it also holds that a low amount of inflation (about 2% annually) is actually good and that zero percent inflation is bad, and deflation, even worse.

While not all mainstream thinkers necessarily agree on why a little bit of inflation is good -- in fact, necessary for a healthy economy -- nevertheless there are several main arguments often used to support it. Below are those main arguments along with their refutations.

1. "Deflation causes buyers to delay purchases, which hurts the economy."

The most fundamental explanation for why deflation is allegedly bad is rooted in a belief about human psychology. According to the theory, when prices consistently go down, people expect more price decreases and wait for them to go down even further. For reasons already discussed, these delayed purchases hurt businesses, employees, and thus ultimately consumers. The process can form a repeated cycle of economic destruction, like the one described two sections above, called a "deflationary spiral."

It's certainly true there are times when expected price drops cause us to delay buying. People delaying certain purchases until the after-Christmas sales are a good example of this. But does such behavior towards deflation always, or even usually, ring true? Oftentimes, when the price of something falls, especially if substantially, we're motivated to buy it. We might say to ourselves that we should purchase it while it's still on sale. Or we understand that we need to purchase it because at that price it won't be in stock for long. These considerations occur because usually price drops aren't like those for after-Christmas sales: we typically don't know if a future price drop will occur. Even when we see the price of specific goods, services, or products repeatedly fall, such patterns still don't rise to the level of having certainty or near certainty; they don't happen in a virtually automatic fashion, the way after-Christmas sales do year after year. So, it's reasonable for us to think there's a real risk of missing the lowest-price sale if we don't act now. Therefore, when we see the price of something we want decrease, we usually don't wait around hoping it will fall further.

Also, not only do we not usually know if prices will drop in the future; we don't usually have time to simply wait for prices to drop. We have to buy what we need or want and get on with our lives. So, a "sit and wait" approach to buying is not a typical situation for consumers.

Moreover, it's well understood in economics that it's normal for businesses to reduce prices -- even repeatedly -- in order to increase demand for items that don't sell well, sometimes in effort simply to minimize losses; or to find the right price that will maximize profit through the sum of sales volume and margins; or simply to aim for more market share. It's hard to square how this mainstream understanding of normal economic behaviors doesn't ultimately contradict the mainstream fear behind deflation. If on a large scale, businesses were to conduct these normal behaviors, then the situation suddenly becomes "abnormal," since it would result in general deflation. Put differently, such behaviors are economically "normal" only if they're not that common, which is an oxymoron.

And if these normal behaviors do indeed lead to a Tragedy of the Commons when done to a large enough degree, then why do governments allow businesses, especially large businesses, to pursue extensive price reductions or embark on price wars? After all, they could easily lead to major deflation and trash the economy as competitors respond.

Another, related contradiction is in recognizing that tax increases, no matter how small, put at least some decrease on consumers' desire to spend, while at the same time supporting the mainstream idea that 2% annual inflation is good for the economy. Many people hold those two beliefs, unaware of the underlying inconsistency in doing so. What if inflation for all sales items remained unchanged and sales taxes went up 2% every year instead? For obvious reasons, not too many people would deny that such a tax policy would hurt consumer spending and thus the economy as a whole.

Of course, these inconsistencies in mainstream economic thought and policy don't themselves refute that deflation is bad nor that some inflation is good. To suggest that they do would be an ad hominem fallacy: we would be "refuting" an idea by simply showing that an advocate's belief system doesn't line up as a whole. Clearly that's irrelevant. But the inconsistencies should make us question "deflation is bad" and "some inflation is good," and ask ourselves how strongly we really believe them; and why, if you do believe at least one of them, it (likely) exists with other beliefs that ultimately contradict it. Moreover, since deflationary fears contradict ideas that are more intuitive and generally deemed true at a more fundamental level -- higher prices disincentivize spending and competent businesses adjust prices according to demand -- then truth would seem to be on the other side of the contradiction, not the "deflation is bad" side.

Finally, price increases are often an effective way for people to begin asking whether or not they really need something or whether there are alternatives. Inflation can certainly hurt the motivation to purchase, long-term or permanently.

2. "Deflation usually occurs in poor economic conditions."

Something that gives more credence to the idea that deflation causes us to forgo purchases is that deflation consistently occurs in economic downturns and stagnation. For example, deflation is often given as a factor in causing the Great Depression and Japan's Lost Decade of the 1980s and 1990s.

But just because deflation is usually associated with economic downturns and stagnation doesn't mean it in any way causes those things. Correlation doesn't equal causation. In fact, deflation usually occurs during economic downturns merely as an effect, not a cause: businesses trying to, at the very least, minimize losses by giving consumers an incentive to buy their products. However, why businesses generally would be having more difficulty selling their products is a whole different matter, with many possible causes. The deflation is simply a result of those underlying problems.

Still, the mistake is understandable. When you see something consistently or pretty consistently occur with something else, it's natural to think that there must be some causal connection. At minimum, it's wise to suspect that there's at least a good chance they might be connected.

So, when people have seen the regularity in which deflation is associated with bad or at least poor economic conditions, it's likely that many have tried to explain this by noticing that there are indeed cases when falling prices causes us to delay purchases. Then, from those cases, they infer that such behavior is true in most cases of deflation. And so the argument that deflation generally hampers economic spending, rather than stimulates it, has stood.

3. "Deflation also hurts the economy by forcing businesses to cut profits and/or cut costs in order to lower prices: layoffs or reduced hours occur, adding to less consumer spending; and debt defaults increase, causing banks to restrict lending, thus further slowing the economy."

It's true that lowering prices can cause some companies great hardship, leading to the consequences described above. This is why many companies simply don't engage in things like price competitions and hope that either they can appeal to customers in other ways or for monopolistic conditions in their market.

What's not true is that categorically businesses must either cut profits or business-related costs to lower their prices. Economies of scale (EOS) is a situation when increasing the number of units produced, bought, transported, or stored decreases the cost per unit of those actions respectively. Because of this, the per unit price can be reduced. While the per unit cost decreases, other costs don't have to for the price to drop, and thus employment is unaffected. And profits can stay the same or even increase, depending on how much the business decides to decrease the price and how many units they sell afterwards.

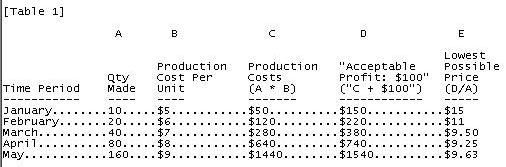

But there's even a situation when a business's per unit cost can stay the same or even increase, and the business can still lower the price without cutting costs elsewhere or reducing its profit. In seller economies of scale (SES), a business can do that simply if it sells more units within a given timeframe or to a certain buyer. Table 1, below, represents a business with a minimum acceptable profit of $100 monthly and without any additional revenue sources. For simplicity, let's also assume that "production costs" are total costs (i.e., all costs required for the product to exist).

The lowest possible price falls for several months, despite the per unit cost continuing to increase. That can occur simply because the business sells more units each month; it has more units with which to make its lowest "acceptable profit." No cost or profit cut is needed.

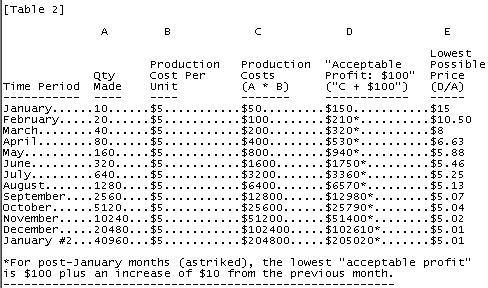

A business can even increase its target profit while lowering prices and not cutting any costs. Table 2 shows an SES example in which the lowest acceptable profit is $100 plus an increase of $10 each month.

Not every business has the means to accomplish EOS or SES. But those concepts refute the argument that lowering prices is necessarily bad for businesses and therefore bad for the economy. Of course, this doesn't mean that all or even most businesses that can achieve EOS or SES when reducing prices necessarily will. Either out of ignorance of the concepts or simply a desire to maximize shorter-term profits -- possibly hurting their longer-term potential and market share -- some businesses will pursue the common, traditional routes of lower prices through cutting profits and/or business-related costs. Still, free market policies have to allow for such decisions and let the market play out, rewarding businesses that can thoughtfully manage their internal affairs while also providing customers with what they want: lower prices.

4. "Deflation and zero-percent inflation make it harder for central banks to provide stimulus during severe economic downturns."

Central banks typically lower interest rates when there is deflation, since deflation is seen as a sign of a slowing economy. But if there is then a major economic downturn, these deflation-fighting decreases risk leaving central banks with one less tool for stimulating the economy and at the worst possible time. If interest rates have been reduced to a very low number, there's little room for improvement.

But this isn't a problem if deflation itself is not seen as an enemy to be fought, and the focus is on whether it occurs due to bad economic conditions or is a result of good things such as widespread technological improvement, EOS, SES, etc. This preserves interest-rate ammunition for times only when the economy really needs it.

5. "Deflation makes it harder to pay off debts, leading to more defaults and stricter lending conditions as a result."

As already mentioned, one of the arguments for why deflation hurts the economy is that layoffs and reduced hours from price decreases not only lessen consumer spending but also make it harder for borrowers to pay off their debts. But we've seen that neither profits nor business costs need to take hit while prices fall. Businesses can lower prices while avoiding cuts, if they can sell the increased units necessary for that to happen.

However, another angle for why borrowers are worse off is that the real value of one's debt increases as prices decrease: the value of one's debt represents more goods and services. But why should that matter? When prices are lower, a smaller amount of your income can go towards your necessities and a larger amount towards paying off your debt. So, unless one is paying their debt through the kinds of things that are dropping in price -- which isn't a common route debts are paid, anyway -- deflation makes it easier to pay debts rather than harder.

Anti-Inflation Factors & Why Inflation is Hard to Predict

The language used so far has been cautious, with phrases such as "tends to" and "more likely" and "greater chance." The actual impact or direction inflation takes is hard to predict mainly because of four factors that can either slow, neutralize, or reverse inflation or its effects.

One of these factors is simply that people can choose. Like the other social sciences, economics has the challenge of studying things with free will. So, you simply can't say with certainty or near certainty that someone will pass their inflation onto another. For instance, even during high inflationary times, some businesses might not only refrain from raising their prices but even lower them -- a move that would not only pleasantly surprise consumers but likely catch many of their competitors off guard. However, even though such things might happen, the incentive or need to pass on inflation is strong. Still, which way will businesses choose?

Two, wages don't stay stagnant for everyone. When someone's wages go up, it can have a psychological effect similar to when prices stay the same or decrease, depending on the context. So if someone's wages increase the same or more than the price increases they experience, there is a good chance that their spending will stay the same or increase despite the inflation. If the wage hike isn't compensatory to inflation, it will still probably weaken any negative behavior. While the spending of wage hike earners likely won't save the whole economy from inflation's effects, it will at least make the effects milder to some extent. (But further complicating this are situations when the wage hikes amidst inflation cause some of those businesses to increase their prices.)

Third, most people have some type of financial leverage. At least in the short term, when the debt is manageable and acceptable to the borrower, this has an effect similar to a wage hike.

Fourth, while inflation is happening, usually deflationary forces are occurring as well. Businesses (or even entire industries) discover cheaper ways to do things, sometimes as desparate responses to inflation, but often as a means to gain a price advantage over their competition.

Yet, despite these difficulties, it's not as if we're totally in the dark. Other factors remaining equal, we know that budgets are more strained when prices increase. And we can see that this increases the incentive or need for others to raise their prices afterwards -- economic data and most people's personal experiences offer further support for these general facts. Those facts don't give us a crystal ball for where inflation will head in a particular timeline. But they do tell us about the risks of inflationary policies.